One of the main drivers of real estate prices is the availability and structure of credit. Mortgage loans are the credit used to finance residential real estate purchases. Government policies, economic conditions, and banking regulations significantly influence the availability and cost of mortgages. While owning a home outright is appealing, most homebuyers rely on mortgages to finance their purchases. Mortgages allow buyers to purchase homes that would be out of reach if they had to pay the full price upfront. By spreading the cost over many years, mortgages increase buyers’ purchasing power, which can drive demand and, consequently, prices. Analysts frequently compare historical property values to median income, not realizing that the property market structure has changed.

Historically, houses were built by their residents or purchased directly with cash or cash equivalents. In the early American colonial period, mortgages were far from standardized. Homeownership was a privilege enjoyed by a select few, as mortgages were typically short-term, with a final balloon payment. For example, land transactions often included agreements that could be likened to modern mortgages, but these were short-term, usually spanning from 5 to 7 years. Further, at the end of this term, the borrower needed to either pay off the remaining balance or refinance—an option fraught with difficulty due to the economic volatility of the time.

The Great Depression of the 1930s exposed critical issues with short-term, balloon-payment mortgages, resulting in widespread foreclosures as homeowners couldn’t manage the large final payments amid economic collapse. This crisis prompted significant government action, creating regulatory agencies and introducing the 15-year self-amortizing mortgage where payments included principal and interest, thus eliminating the balloon payment. This was later followed by additional changes, such as the federal government insuring mortgages to reduce lender risk and encourage longer-term loans, initially set at 20 years but soon extended to 30 years.

These government interventions fundamentally transformed the U.S. mortgage landscape. Today, the 30-year fixed-rate mortgage dominates, but the market now offers diverse options like adjustable-rate mortgages (ARMs) and various government-backed loans. The mortgage revolution has significantly affected how property is bought and its market value. Because of the modern mortgage and its popularity, most home buyers don’t base their purchase decision on the absolute value of a home but on the monthly payment. In turn, the two primary determinants of the monthly payment are the interest rate and loan term.

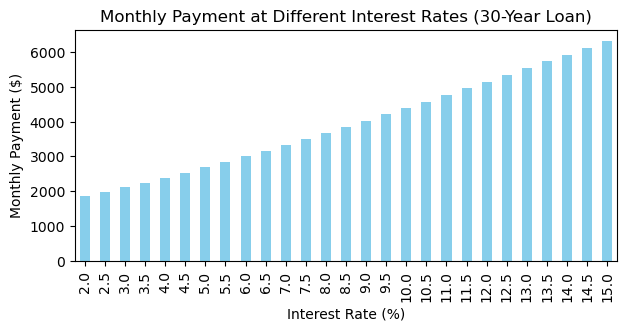

Let’s take a look at an example. For apple-to-apple comparisons, all values will be calculated based on a $500,000 mortgage with a $0 down payment.

- Interest rates: A $500,000 loan at 4% and 8% equates to an annual payment (including principal) of $28,645 and $44,026, respectively. Monthly, that equates to a $2,387 and $3,669 monthly payment, quite the difference.

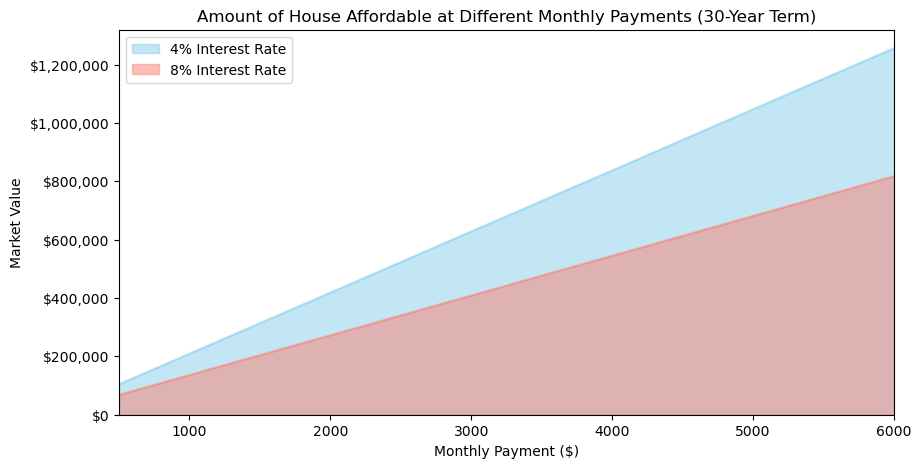

Lower interest rates improve housing affordability by lowering the monthly payment, which drives up demand and home prices. Assuming stable wages, one can pay 50% more for a house at 4% than an 8% interest rate. This is because a $750,000 loan at 4% has a similar monthly payment as a $500,000 loan at 8%. If a family can afford a $3,600 monthly payment, a 4% 30-year loan can buy them a home worth $754,060. With an 8% loan, they can buy a home worth $490,620.

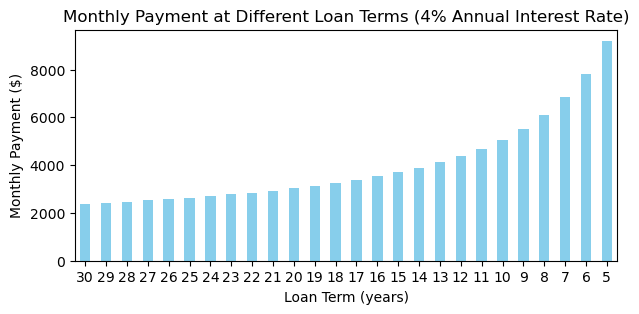

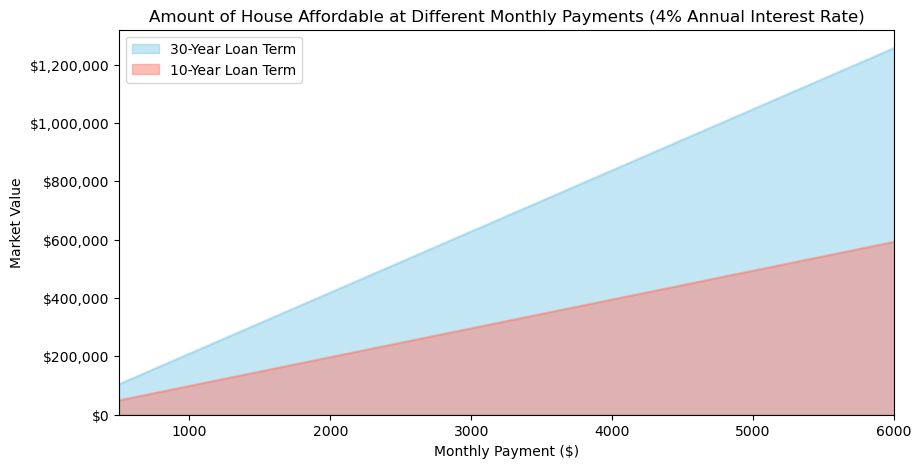

- Mortgage term: Longer-term mortgages allow buyers to reduce their monthly payments, making home buying more accessible. Similarly, this can drive up demand and prices. Let’s look at the numbers:

- A 30-year mortgage at a 4% interest rate has an estimated annual payment of $28,645 or $2,387 monthly (including principal payment).

- A 10-year mortgage at a 4% interest rate is estimated to have an annual payment of $60,747 or $5,062 monthly (including principal payment).

Hence, longer loan terms improve housing affordability. Assuming wages are stable, one can pay more than double for a house with a 30-year loan than a 10-year loan term. If a family can afford a $3,600 monthly payment, a 30-year loan allows them to buy a property worth $754,060, while a 10-year loan allows them to afford only a $355,572 property.

Over the last 100 years, the duration of U.S. mortgage loans has increased from below 10 years to the current 30-year mortgage in the United States. This has led to a permanent increase in home values relative to incomes. While the 30-year fixed-rate mortgage is a cornerstone of the American housing market, it’s less common in other parts of the world. In many other countries, mortgage systems feature shorter terms, adjustable rates, or a combination. For example, the average loan term in Europe is between 20 and 30 years. However, some countries do offer mortgages that extend beyond the 30-year mark. Terms up to 50 years are available in Spain and France, and Finland has an option for a 60-year product, though these longer-term products have a low market share. At the extreme, Japan and Switzerland have offered 100-year intergenerational mortgage products. There is no reason to believe that the 30-year mortgage will be the last increase in the loan term since governments can extend it further if they want to stimulate the property market.

Mortgages are increasingly becoming the preferred method of purchase for home buyers, which means that home buyers base their decisions on payment affordability, not absolute real estate values. Frequently, analysis of historical affordability looks at absolute property prices adjusted for inflation or prices relative to income, ignoring the structure of credit (interest rates and loan duration). Assuming loan duration is stable, interest rates are the primary tool influencing property values.

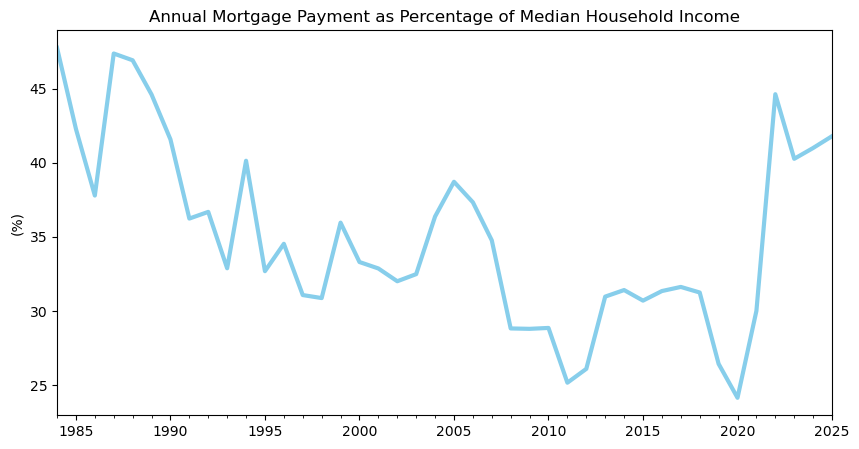

For example, given that the 30-year mortgage has been the dominant term in the U.S. for over 40 years, we can compare the historical annual mortgage costs divided by median household income. We can see that mortgage costs were high in the late 1980s, mid-2000s, and early 2020s. Real estate prices declined following the prior two periods. Hence, in the 2020s, mortgage rates must come down, and/or incomes must rise, or property prices will have to fall.